Image

AARP Getty Images

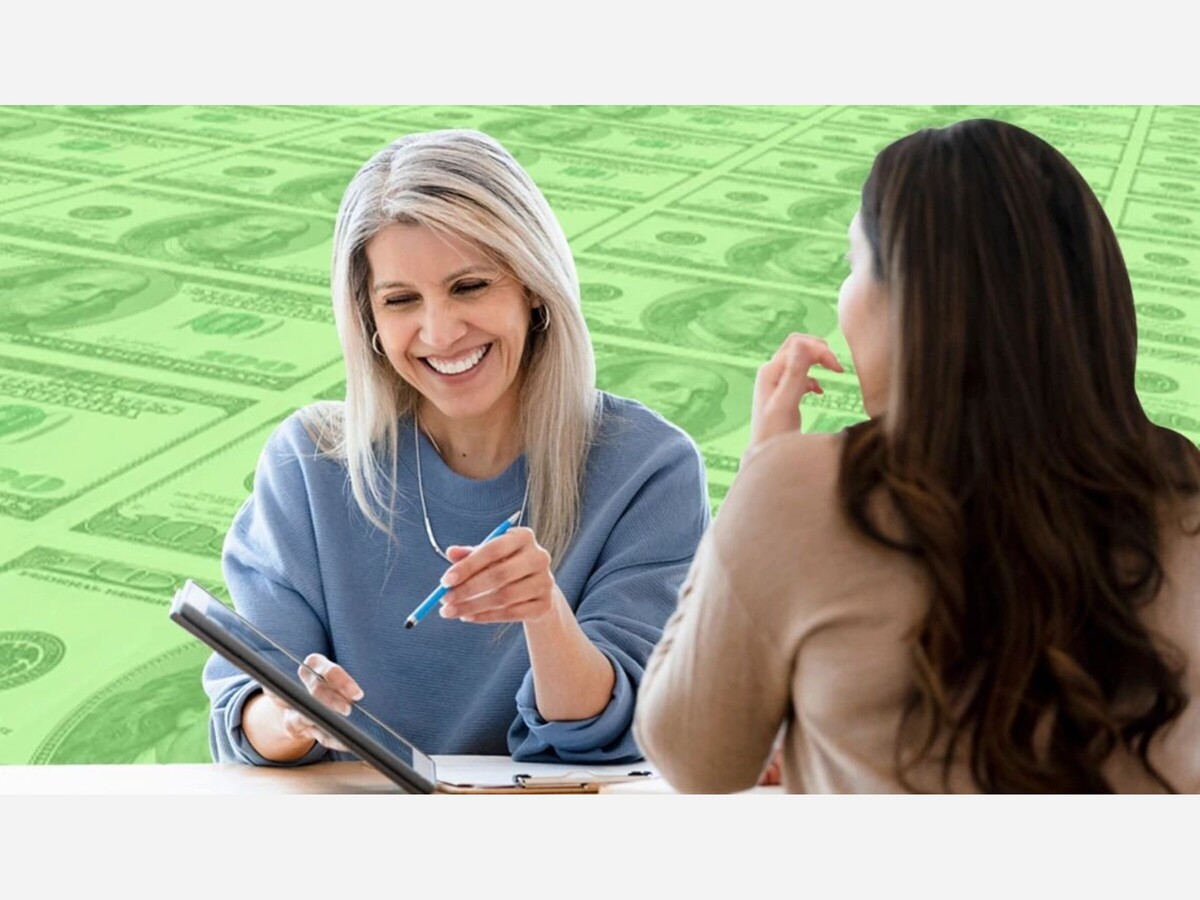

Michael Hunsberger had spent 25 years in the U.S. Air Force, working on communications and cybersecurity, and was approaching retirement. As he thought about what he wanted to do next, he knew he could move into the private sector and continue in the same field. But Hunsberger had always enjoyed doing his own financial planning and helping friends, so he considered switching to that field. He then learned about a company that helps new financial advisers get their businesses up and running. After he went to a conference and spoke to other members of the military who had made the switch to being personal financial advisers, he was sold.

Hunsberger started Next Mission Financial Planning in St. Charles, Missouri, in 2021. He says being a financial planner could be a good second career for people who have done their own financial planning and enjoyed it. “If you’ve been a do-it-yourselfer, and you really enjoy getting into the nuances and understanding everything about financial planning, and you just enjoy working with people,” he says, this might be an ideal option for you.

Becoming a personal financial adviser as a second career — particularly in your 40s, 50s or 60s — can be especially advantageous, says Ivan Illán, founder and chief investment officer of Aligne Wealth Advisors Investment Management, an investment advisory firm based in Los Angeles, and author of Success as a Financial Advisor for Dummies. “There is a real advantage to coming into this business later in life,” he says. Having work and life experience, as well as a personal and professional network, can help new financial advisers build credibility and a client base, he explains.

The personal financial adviser sector is expected to grow 13 percent between 2022 and 2032, which is much faster than the average job category, according to Bureau of Labor Statistics data, with median pay at roughly $100,000 per year.

A variety of professionals call themselves financial planners. They include brokers, accountants, insurance salespeople, investment advisers and others who work in the financial services industry.

You can build your business in a variety of ways, depending on your preferences and area of specialization, Illán says. You may want to offer investment advice and conduct securities transactions, like buying and selling stocks and bonds for clients. You may also wish to sell insurance products that offer guaranteed income, called annuities, or other types of insurance that can help protect assets.

Financial advisers can be salaried employees or independent contractors, depending on where they work, says Melissa Sotudeh, managing director and chief compliance officer at Halpern Financial, Inc., a financial advisory firm based in Ashburn, Virginia.

Sotudeh had worked for the Securities and Exchange Commission (SEC), which regulates the securities sector, before being a stay-at-home mother for a decade. Her children were still young, so she was looking for a career option that had flexible hours. Sotudeh spotted an ad in The Washington Post. “It said ‘Financial planner position, school hours,’ ” she recalls. “That was perfect.”

Even though she had worked in securities regulation, she wasn’t familiar with the role of financial planner. She quickly learned about it, and the thought of helping people get on the right financial track appealed to her. Since then, she has built a thriving career and helped grow a firm.

If you’re interested in becoming a financial adviser after age 50, here are some important steps you’ll need to take.

Illán advises those who are looking at building their own business to provide a range of financial services. “You really want to have all of the tools available to yourself so you can serve a wide variety of financial needs,” he says. “Clients really want a competent one-stop shop. They would love to be able to get all of their advice from one particular adviser.”

While some advisers are fee based, others earn income from commissions on the products they sell, Illán adds. Offering a variety of products can provide multiple revenue streams.

Depending on the products and services you want to provide — selling securities or insurance, or giving investment advice — you’ll need to pass exams or secure the appropriate licenses.

Securities professionals must pass one or more exams administered and overseen by the federal Financial Industry Regulatory Authority (FINRA).

Professionals who wish to sell insurance may need to be licensed by their state. The National Association of Insurance Commissioners publishes a directory of state insurance departments.

To obtain the certified financial planner (CFP) designation, financial advisers undergo a rigorous course of study and pass the exam. They must adhere to a code of ethics and satisfy continuing education requirements.

There are many certifications and specializations available, so speak to people in the industry to determine which are best for you.

To obtain certain licenses and accreditations, you will need to work for a financial services or registered investment advisory (RIA) firm and be sponsored or otherwise gain experience. The Series 7 exam, which assesses competency to sell securities, requires sponsorship by a FINRA member firm or self-regulatory organization. Credentials like the CFP or registered financial consultant (RFC) often require many hours of experience or a completed apprenticeship.

In addition to building a financial planning career based on products and services offered, some financial advisers focus on providing advice to specific types of customers. If you decide to go that route, drawing on your own experience and network can be helpful.

For example, Sotudeh works with many business owners and high-net-worth individuals. Hunsberger has found that his military background gives him insight into the needs of military families.

“I work mainly with military and veterans across the country,” he says. “If you’re more interested in having an in-person practice, it’s probably easier to get the word out locally. It really depends on what you’re interested in doing and who you’re interested in trying to help.”

Illán advises new financial planners to observe their personal strengths in the business, especially in the first year. “You’re really developing your specific value proposition,” he says. He estimates that the first three years are crucial to establishing that understanding and building a client base that will help your business last.

Hunsberger found that attending conferences and engaging the services of a company that helps new financial planners launch their own firms was helpful in starting his business.

Sotudeh says the role has evolved over the two decades she has been working in it. “It’s not as much sales, as people sometimes misconstrue it. There can be a business development aspect, but the heart of it is you’re listening to personal finance situations, and you’re trying to provide guidance and customized solutions,” she says. She adds that helping people in this way can be enormously rewarding.

Gwen Moran is a contributing writer for AARP who specializes in business and finance. Her work has appeared in many leading business publications and websites, including Entrepreneur, Kiplinger.com, Newsweek.com, and the Los Angeles Times Magazine.

Partly Cloudy, with a high of 88 and low of 65 degrees. Sunny during the morning, partly cloudy during the afternoon, clear overnight.

wow .

What a beautifully written reflection on an unforgettable performance. You could really feel the emotion and atmosphere of the evening through every paragraph, especially the way the cello performance was described.